This report, our fourth in a series of articles on activity based business analysis and performance for US gases and welding distributors, examines distribution costs and improving distribution efficiency through Activity Based Costing (ABC).

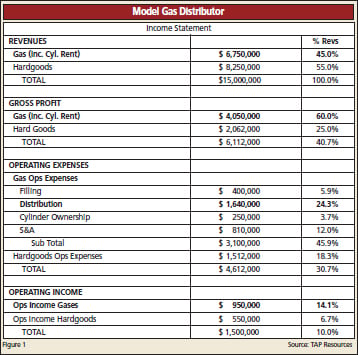

We introduced a model P&L for a hypothetical distributor in our first article. We use it here once again, this time to discuss gases and cylinder delivery cost components as part of total operating expenses. (For the previous three articles in this series see “Impacting Your Bottom Line,” CGI, March 2009; “Activity Based Accounting for Distributors,” CGI, April 2009; and “Activity Based Costing for Distributors,” CGI, June 2009.)

WHAT GETS MEASURED GETS DONE

Gases and welding distributors transport gas and hardgoods products to the customer directly, using their own transportation. This article focuses on the delivery of gases and assumes that delivering hardgoods, if done at all, is an insignificant part of this distributor’s trucking costs, and does not affect miles driven or stops made. We begin our discussion on efficiency with my favorite axiom — “What gets measured and displayed is what gets done.”

... to continue reading you must be subscribed