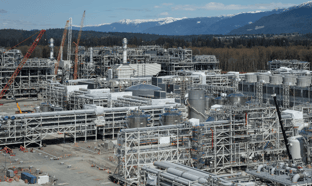

New US LNG export projects face stiff headwinds

Like many businesses, the US liquefied natural gas (LNG) industry spent most of 2020 in a state of financial quarantine. As Covid-19 spread through gas-importing nations in Europe and Asia, global LNG demand fell, prices plummeted – and major US liquefaction facilities stood mostly idle for the summer, their capacity neither needed nor wanted. Even though federal regulators have granted permits to 16 new LNG export projects, not a single one has completed financing in almost two years.

Yet we’re now hearing speculation about a new round of US LNG construction. Global LNG prices spiked to multi-year highs during last winter’s Asian cold snap, rekindling optimism, and spiked to all-time highs this fall. US LNG plants operated at nearly full capacity for much of the year. Now, say the boosters, all the new projects need is some firm commitments from long-term buyers, and they’re off to the races.

Exhibit A is Tellurian, Inc., which recently secured 10-year purchase commitments from Shell and two trading houses for its proposed Driftwood LNG plant in Louisiana. Time will tell whether these contracts will attract the financing needed to get the project off the ground. In the past, lenders demanded longer-term contracts with guaranteed liquefaction fees, rather than Driftwood’s shorter-term agreements tied to volatile international price indexes. But before they can secure the types of stable, blue-chip contracts that lenders prefer, new LNG projects will have to navigate four troublesome market headwinds that are weakening the industry’s momentum.

... to continue reading you must be subscribed